20-F: Annual and transition report of foreign private issuers [Sections 13 or 15(d)]

Published on April 4, 2025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

or

For the fiscal year ended December 31 , 2024

or

For the transition period from/to

or

Date of event requiring this shell company report:

Commission file number 333-284251

(Exact Name of Registrant as specified in its charter)

Not applicable

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone: (757 ) 858-6500

E-mail: JChristy@titanamerica.com

(Name, Telephone, E-mail and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class |

Trading Symbol(s) |

Name of Each Exchange on Which Registered |

||||||||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report:

Not applicable

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes☐ No ☑

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☐ |

Large accelerated filer |

☐ |

Accelerated filer |

☑ | Emerging growth company |

|||||||||||||||||||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP |

☐ | ☑ | Other |

☐ | |||||||||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 |

☐ | Item 18 | ☐ |

|||||||||||||||||

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes |

☐ | No |

☑ |

|||||||||||||||||

TABLE OF CONTENTS

NOTICE REGARDING DISCLOSURE OF MINING PROPERTIES

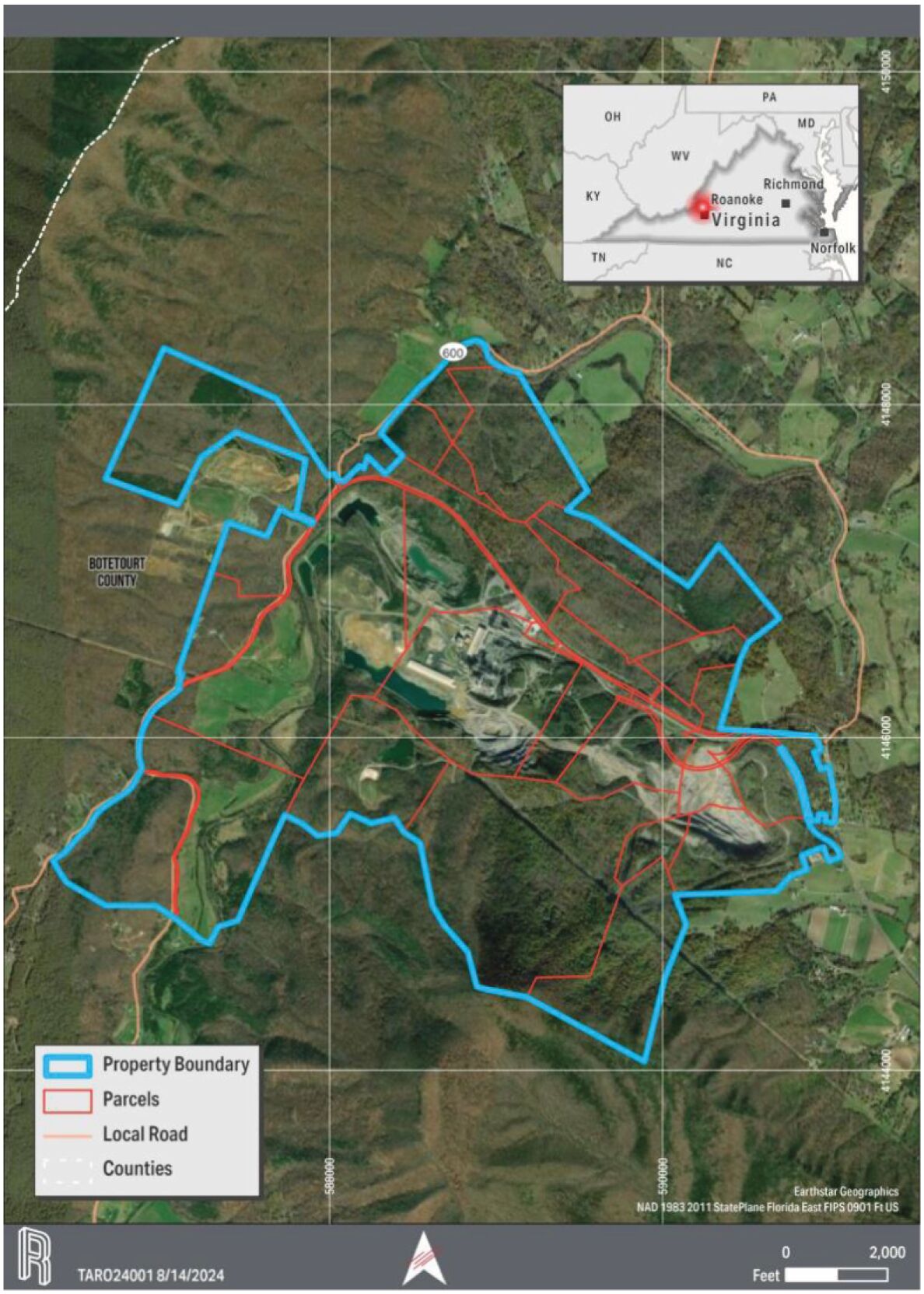

The technical report summary for Pennsuco Quarry, Miami-Dade County, Florida and the technical report summary for Roanoke Quarry, Botetourt County, Virginia, included herewith, have been prepared in accordance with subpart 1300 of Regulation S-K –Disclosure by Registrants Engaged in Mining Operations, (“S-K 1300”) as issued by the U.S. Securities and Exchange Commission (the “SEC”), under the United States Securities Act of 1933, as amended, (the “Securities Act”), which governs disclosure for mining registrants. Such technical report summaries titled “Technical Report Summary for Pennsuco Quarry, Miami-Dade County, Florida” and “Technical Report Summary for Roanoke Quarry, Botetourt County, Virginia” respectively, each dated August 30, 2024, were prepared by Continental Placer Inc., independent geological and environmental consultants, who is a qualified person under S-K 1300 and is independent of us, are included as Exhibit 96.1 and Exhibit 96.2, respectively, in this Annual Report.

Unless otherwise indicated, the scientific and technical information contained in this Annual Report regarding the Pennsuco Quarry and Roanoke Quarry have been derived from the S-K 1300 Report, which was included as Exhibit 96.1 and Exhibit 96.2, respectively, to our registration statement on Form F-1 filed with the SEC and declared effective on February 6, 2024, and is included as Exhibit 96.1 and Exhibit 96.2, respectively, to this Annual Report (our “Registration Statement”).

2

Cautionary Statement Regarding Forward-Looking Information

This document contains “forward-looking statements,” as that term is defined in the U.S. federal securities laws, concerning our business, operations and financial performance and condition, as well as our plans, objectives and expectations for our business operations and financial performance and condition. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “due,” “estimate,” “expect,” “goal,” “commit,” “commitment,” “intend,” “may,” “objective,” “plan,” “predict,” “potential,” “positioned,” “pioneer,” “seek,” “should,” “target,” “will,” “would” and other similar expressions that are predictions of or indicate future events and future trends, or the negative of these terms or other comparable terminology.

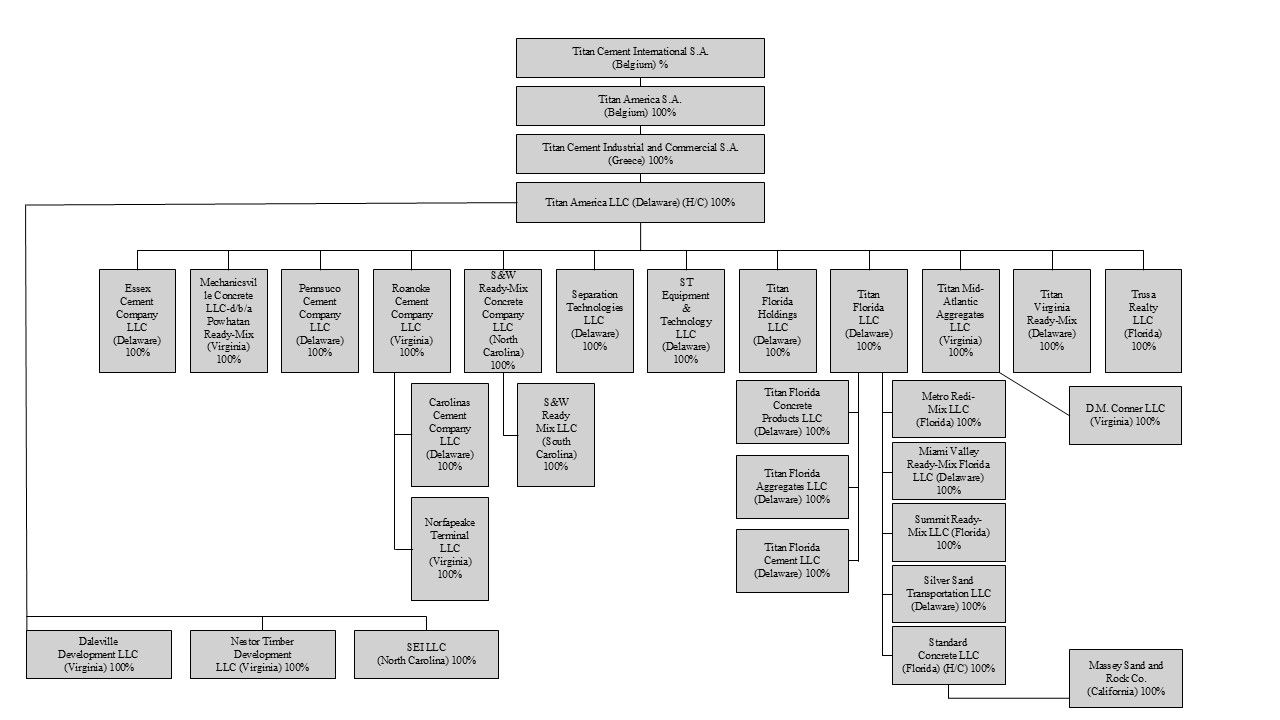

In this document, Titan America SA and its consolidated subsidiaries are together referred to as the “Company,” “Titan America,” “we,” “us,” “our” or similar terms. Titan Cement International SA, Titan America’s ultimate parent, is referred to as “Titan Cement International,” “TCI,” or “our Parent.”

From time to time, oral or written forward-looking statements may also be included in other materials released to the public. These statements are based on management’s assumptions, judgments and beliefs in light of the information currently available to it. Titan America cautions investors that a number of important risks and uncertainties could cause actual results to differ materially from those discussed in the forward-looking statements, and therefore investors should not place undue reliance on them. Investors also should not rely on any obligation of Titan America to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Titan America disclaims any such obligation. Risks and uncertainties that might affect Titan America include, but are not limited to:

•increases in the cost or fluctuations in the availability of labor, fuel and energy, raw materials and other production inputs;

•fluctuations in energy, fuel prices and transportation costs and changes in prices for or availability of commodities, labor or other production inputs;

•increases in market demand for cement substitutes;

•impacts of climate change and regulations intended to address climate change;

•fluctuations in public spending for infrastructure and large-scale projects, construction levels and urbanization trends;

•the timing or likelihood of regulatory approvals, licenses and permits, as well as delays in construction projects;

•our ability to protect our intellectual property, the confidentiality of our know-how, trade secrets, technology and other proprietary information;

•regulatory developments in the United States, Europe and other jurisdictions, including those relating to the protection of the environment, health and safety;

•our expectations about market trends;

•our ability to accurately forecast demand for our products and manage our inventory;

•developments relating to our competitors and our industry, including demand for cement substitutes;

•our ability to effectively manage our anticipated growth;

•our ability to attract and retain key management and other qualified personnel;

•union disputes and other employee relations issues;

3

•our ability to realize the anticipated benefits of strategic investment in research and development, digitalization and logistical capabilities;

•the future trading price of our common shares and impact of securities analysts’ reports on these prices;

•the risk that an active, liquid trading market for our common shares may not develop or that the market for our common shares may be volatile;

•increased costs and regulatory burdens resulting from being a public company listed on the New York Stock Exchange (“NYSE”);

•our ability to operate as a standalone public company;

•conflicts of interest and disputes arising between Titan Cement International and us that could be resolved in a manner unfavorable to us;

•our ability to remediate the identified material weaknesses in our internal control over financial reporting; and

•other risks and uncertainties, including those listed under the caption “Risk Factors.”

We caution you that the foregoing list does not contain all of the forward-looking statements made in this document.

You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this document primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors, including those described above, in “Risk Factors” under “Item 3. Key Information ,” “Item 4. Information on the Company ,” “Item 5. Operating and Financial Review and Prospects,” “Legal Proceedings” included in “Item 8. Financial Information,” Titan America’s consolidated financial statements referenced in “Item 8. Financial Information” and “Item 11. Quantitative and Qualitative Disclosures about Market Risk.” Moreover, we operate in a competitive environment, and new risks and uncertainties may therefore emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this document. We cannot guarantee that the results, events and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

Neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements. Moreover, the forward-looking statements made in this document relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this document to reflect events or circumstances after the date of this document or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this document, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely upon these statements.

The forward-looking statements contained in this document are excluded from the safe harbor protection provided by the Private Securities Litigation Reform Act of 1935 and Section 27A of the Securities Act.

All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this special note. Additionally, our discussion of various information, including ESG matters, both here and in other locations is

4

information by various standards and the interests of various stakeholders. As such, not all such information may be material and references to “materiality” and any related assessment of ESG “materiality” may differ from the definition applicable for relevant reporting purposes.

5

__________________________________________________________________________________________________________

Item 1. Identity of Directors, Senior Management and Advisers

Not Applicable

Item 2. Offer Statistics and Expected Timetable

Not Applicable

Item 3. Key Information

A. [Reserved]

B. Capitalization and Indebtedness

Not Applicable

C. Reasons for the Offer and Use of Proceeds

Not Applicable

D. Risk Factors

This section contains forward-looking statements that are subject to the Cautionary Statement Regarding Forward-Looking Information appearing earlier in this annual report. Risks to Titan America are also discussed elsewhere in this annual report.

Risks Related to Our Business and Industry

We have been, and may continue to be, adversely impacted by volatility and seasonality in the U.S. residential and non-residential construction markets.

Our business is largely dependent on demand for residential construction, public spending levels for infrastructure and large-scale projects. The U.S. residential and non-residential construction markets are volatile and subject to cyclical market pressures. The level of activity in the U.S. residential and non-residential construction markets is based on numerous factors such as availability of credit, interest rates, general economic conditions, consumer confidence and other factors that are beyond our control. As a result of macroeconomic headwinds we have faced over the past several years, such as prolonged inflationary cost pressures, supply chain disruptions, the impact of public health crises and geopolitical conflicts, U.S. residential and non-residential construction markets have been adversely affected, and may continue to be adversely affected in the future, by changes in the cost of raw materials as well as labor costs, energy costs and freight costs associated with transportation of raw materials. In addition, demand for our products could decline if companies and consumers are unable to obtain financing for construction projects or if an economic recession causes delays or cancellations to infrastructure projects. A significant downturn in activity in either the U.S. non-residential or residential construction markets could have a material adverse effect on our business, financial position, results of operations and cash flows.

We cannot predict the market conditions that will impact the residential or non-residential construction industry or the timing of residential or non-residential construction activity. We also cannot provide any assurances that the operational strategies we have implemented to address current market conditions will be successful. Weakness in the non-residential or residential construction industry could have a material adverse effect on our business, financial position, results of operations and cash flows. Due to the potential volatility in the residential and non-residential construction markets, there may be fluctuations in our operating results, and the results for any historical period may not be indicative of results for any future period. Any uncertainty about current economic conditions can pose a risk to our business, financial position, results of operations and cash flows, as participants in the U.S. non-residential and residential construction industries may postpone spending in response to tighter credit, negative financial news or declines in income or asset values, which could have a material negative effect on the demand for our products.

6

__________________________________________________________________________________________________________

A significant portion of our business is seasonal, with results of operations affected by weather conditions. For the Mid-Atlantic region, construction material production and related contracting services typically follow the activity in the construction industry, with heavier workloads in the spring, summer and fall. Accordingly, we typically experience a decrease in sales in our Mid-Atlantic reportable segment during the first and fourth quarters reflecting the effect of the winter season in North America and an increase in sales in the second and third quarters reflecting the effect of the summer season in North American markets. Besides the seasonal effects of weather conditions, extreme or unusually adverse weather conditions, which have occurred and may reoccur, such as extreme temperatures, heavy or sustained rainfall or snowfall, wildfires, hurricanes and storms may affect the demand for products and the ability to perform services on construction work. Heavy or sustained rainfall may particularly impact operations of our ready-mix concrete business. Extreme or unusually adverse weather conditions could negatively affect our results of operations, financial position and cash flows.

Fluctuations in energy, fuel prices and transportation costs could have an adverse effect on our costs of goods sold.

A significant proportion of our cost of goods sold are incurred in connection with the consumption of thermal and electric energy necessary to produce our products, and in connection to transportation costs incurred for the distribution of our products. Cement production consumes a large quantity of energy, especially for the kilning and grinding processes.

Energy is also required for the transportation, both within our facilities and externally, of our products through our trucks in addition to the operation of our equipment. The principal elements of these energy costs are fuel expenses and electricity expenses (which include, inter alia, costs for coal, petroleum coke, natural gas and alternative fuels). Due to their size and weight, aggregates are costly and difficult to transport efficiently. Our products and services are generally localized around our aggregate sites and served by truck or in certain markets by rail or barge. We could be negatively impacted by freight costs due to rising fuel costs; rate increases for third-party freight; truck, railcar or barge shortages, including shortages of truck drivers and rail crews; rail service interruptions; and minimum tonnage requirements, among other things. To the extent price increases or other mitigating factors are not sufficient to offset these increased costs adequately or timely, or if the price increases result in a significant decrease in sales volumes, our results of operations, financial position and cash flows could be negatively impacted. Increases or significant fluctuations in energy and fuel costs, freight rates or other transportation costs could adversely affect our results of operations, business and financial condition, especially if we are unable to pass along higher input costs to our customers. Energy prices may vary significantly in the future, largely due to market forces and other factors beyond our control, including changes in the relevant regulatory regime or governmental policy applicable to energy prices. We may also, particularly in the case of coal, experience time lags between movements in energy prices and movements in production costs since the supply of a substantial proportion of energy resources is secured pursuant to long-term purchase agreements. Risks related to fluctuations in energy and fuel costs are increased due to the fact we do not use any long-term hedging instruments to mitigate the effects of such fluctuations. Legal requirements, as well as a heightened awareness of environmental sustainability, have placed increased pressure on energy-intensive industries such as the cement industry to increase their energy efficiency and to transition to more environmentally friendly sources of energy, such as renewables, which could further increase our cost of goods sold. Changes in the availability of energy sources to meet these demands could adversely impact our ability to operate, and changes in energy prices as a result could significantly increase our operating costs.

Significant changes in prices for or availability of commodities, labor or other production inputs could negatively affect our costs of goods sold.

Our manufacturing operations are exposed to fluctuations in costs for labor, energy and raw materials, among other things. These inputs are also subject to supply chain fluctuations and other general economic and market conditions beyond our control. However, the primary key raw materials used in the manufacturing of cement or aggregates are controlled through a combination of owned and leased reserves. Since 2021, we have experienced elevated commodity and supply chain costs and other inputs used in the production and distribution of our products and services. Recent inflationary pressures have increased our costs above historical averages.

Availability of key natural resources used in the manufacturing of our products is one of the factors that significantly affect our operations and profitability. Therefore, continued active management of our quarries and production plants and the related permits, licenses, rights and titles is key to controlling manufacturing cost escalations in the long term. While the primary source of the key raw material of limestone is from owned reserves adjacent to the cement plants, there can be no assurance that we will be able to maintain or renew these land and mining rights or that we will have similar cost containment for other inputs used in the production process.

7

__________________________________________________________________________________________________________

Our access to natural resources could be adversely affected by the closure of one or more of our quarries due to unforeseen circumstances related to changes in regulatory environment, disruptions to available transportation networks, or the cancellation of freight agreements or other key contract terminations. If any of our suppliers ceases to operate, or if we would need to incur additional costs to obtain such materials from other sources, such limitations on our ability to obtain the various inputs required, or to obtain those inputs without additional costs, could have a material adverse effect on our results of operations. Moreover, as we pursue less carbon-intensive inputs for cement, we may experience similar difficulties with alternative inputs such as supplementary cementitious materials (“SCMs”).

Increased market demand for cement substitutes could have an adverse impact on our business.

We specialize in the production of cement, aggregates, ready-mix concrete and related products and derive substantially all of our revenue therefrom. Materials such as wood, steel, gypsum, plastic, aluminum and ceramics can be used in construction as a substitute for cement. Other existing construction techniques, such as the use of drywall, as well as any new construction techniques and modern materials, could decrease the demand for cement, ready-mix concrete and mortars. In addition, new construction techniques and modern materials that could replace the use of cement may be introduced in the future. To the extent such products are perceived as having superior environmental or other sustainability characteristics, this may cause customers to be more willing or quick to replace their use of cement. The use of substitutes for cement could cause a significant reduction in the demand and prices for our products and may have a material adverse effect on our business, results of operations and financial condition.

We operate in a highly competitive industry.

The markets for cement, aggregates and other construction materials and services are very competitive. Competition in these segments is based largely on price and on the quality of the material, service provided, logistics and innovative solutions offered. Similarly, our products are fairly commoditized and our ability to price them in a profitable manner is constrained by a competitive price environment, restricting our profitability levels. Competition, whether from established market participants or new entrants, could cause us to lose market shares, increase expenditures or reduce pricing, any one of which could have an adverse effect on our business, results of operations or financial condition.

We compete in each of the markets in which we operate with domestic and international cement producers, as well as importers. Each of these markets we serve are highly fragmented and we compete with a number of regional and national companies. These producers may have greater financial and other resources than we do. Some others are smaller and more specialized and concentrate their resources in particular areas of expertise. We could face increased competition, which would result in lower prices and decreased volumes, either from existing players or new entrants to the markets in which we operate. Further, our profitability is generally dependent on the level of demand for such building materials and services as a whole as well as on our ability to maximize efficiencies and control operating costs. Prices in these markets are subject to material changes in response to relatively minor fluctuations in supply and demand, general economic conditions and other market conditions beyond our control.

In order to maintain or further reinforce our competitive position, we rely on periodic investments in the areas of production and innovation, and on regular maintenance of our production facilities. In the future, we may not have adequate resources to continue to make such investments, and, as a result, may not be able to continue to successfully compete in the markets in which we operate. In addition, competitors could react more quickly to the changing needs of customers, differentiate themselves more effectively, or improve the functionality or performance of their products more quickly than us or in a more cost-effective manner. Therefore, we may face significant price, margin or volume declines in the future, which could have an adverse effect on our business, results of operations or financial condition in particular in markets where cement overcapacity or oversupply is prevalent.

A material disruption at one or more of our facilities or in our supply chain could have a material adverse effect on us.

We own and operate manufacturing facilities of various ages and levels of automated control and rely on a number of third parties and affiliates as part of our supply chain, including for the efficient distribution of products to our customers. Any disruption at one of our manufacturing facilities or within our supply chain could prevent us from meeting demand or require us to incur unplanned capital expenditures. Older facilities are generally less energy efficient and are at an increased risk of breakdown or equipment failure, resulting in unplanned downtime. Newly commissioned facilities are also subject to unforeseen breakdowns or failures related to mistakes in engineering and equipment selection, poor workmanship during fabrication and/or installation, accidents during the construction and/or commissioning phases, mistakes during initial operation and other related issues that can cause significant delays in the project implementation and facility start up. Any unplanned downtime at our facilities may cause delays in meeting customer

8

__________________________________________________________________________________________________________

timelines, result in liquidated damages claims or cause us to lose or harm customer relationships. Additionally, we require specialized equipment to manufacture certain of our products, and if any of our manufacturing equipment fails, the time required to repair or replace this equipment could be lengthy, which could result in extended downtime at the affected facility. Any unplanned repair or replacement work can also be very expensive. Moreover, manufacturing facilities can unexpectedly stop operating because of events unrelated to us or beyond our control, including fires and other industrial accidents, floods and other severe weather events, natural disasters, environmental incidents or other catastrophes, utility and transportation infrastructure disruptions, shortages of raw materials, and acts of war or terrorism. Work stoppages, whether union-organized or not, can also disrupt operations at manufacturing facilities. Furthermore, while we are generally responsible for delivering products to the customer, in some instances, we do not maintain our own fleet of delivery vehicles and outsource this function to third parties. Any shortages in trucking or rail capacity, any increase in the cost thereof, or any other disruption to the highway systems, could limit our ability to deliver our products in a timely manner or at all. Any material disruption at one or more of our facilities or those of our customers or suppliers or otherwise within our supply chain, whether as a result of downtime, facility damage, an inability to deliver our products or otherwise, could prevent us from meeting demand, require us to incur unplanned capital expenditures or cause other material disruption to our operations, any of which could have a material adverse effect on our business, financial condition and results of operations. While we maintain insurance policies covering, among other things, physical damage, business interruptions and product liability, these policies may not cover all our losses. In addition, there is no assurance that insurance will continue to be available on terms acceptable to us.

Delays in construction projects and any failure to manage our inventory could have a material adverse effect on us.

Many of our products are used in large-scale construction projects which generally require a significant amount of planning and preparation before construction commences. However, construction projects can be delayed and rescheduled for several reasons, including unanticipated soil conditions, adverse weather or flooding, changes in project priorities, financing issues, difficulties in complying with environmental and other government regulations or obtaining permits and additional time required to acquire rights-of-way or property rights. These delays or rescheduling may occur with too little notice to allow us to replace those projects in our manufacturing schedules or to adjust production capacity accordingly, creating unplanned downtime, increasing costs and inefficiencies in our operations and increased levels of obsolete inventory. Any delays in construction projects and our customers’ orders or any inability to manage our supply could have a material adverse effect on our business, financial condition and results of operations.

Our investments may not result in expanded capacity at our facilities at the expected levels or timeline, or at all, which could result in a variety of inefficiencies in our business and hinder our ability to generate revenue and profits. If our investments do not result in expanded capacity at our facilities at the levels or timeline that is expected, or at all, we could incur additional costs or experience delays.

We have recently expanded, and made significant investments to further expand, the capacity of our various facilities. However, it is difficult to predict whether our investments will result in expanded capacity at our facilities at the expected levels or within the expected timeline, or at all, and we may have limited insight into trends that may emerge and affect our business. If our investments do not result in expanded capacity at the levels or timeline that is expected, or at all, we could incur additional costs or experience delays. Inaccurate predictions regarding these levels or timelines may prevent us from increasing our production levels, thereby hindering our ability to meet higher demands. Failure to increase capacity and meet higher demands may harm our business, prospects, financial condition, results of operations, and cash flows.

The estimates of a multi-year growth phase in our industry included in this document may prove to be inaccurate, and even if the markets in which we operate achieve the forecasted growth, our business could fail to grow at similar rates, or at all, and we could have over-capacity of our products.

The estimates of a multi-year growth phase in our industry included in this document may prove to be inaccurate. Market opportunity estimates and growth forecasts are subject to significant uncertainty and are based on assumptions and estimates that may not prove to be accurate, including as a result of any of the risks described in this document.

The variables that go into the calculation of multi-year growth are subject to change over time, and there is no guarantee that any particular number or percentage of addressable customers covered by the multi-year growth estimates will purchase our products at all or generate any particular level of revenues for us. Even if the markets in which we compete meet the size estimates and growth forecasted in this document, our business could fail to grow at similar rates, or at all, and we could have over-capacity of our products, especially in light of the investments we have made to further expand the capacity at our various facilities. Our growth is subject to

9

__________________________________________________________________________________________________________

many factors, including our success in implementing our business strategy, which is subject to many risks and uncertainties. Accordingly, the forecasts of multi-year growth of our industry included in this document should not be taken as indicative of our future growth.

Any delay or problem with operating or upgrading our existing information technology infrastructure could cause a disruption in our business and adversely impact our financial results.

Our ability to operate our business on a day-to-day basis largely depends on the efficient operation of our information technology infrastructure and our cloud providers, the largest of which is Microsoft Azure. We may be susceptible to hacks into our systems or other security breaches by unauthorized third parties. We are also susceptible to errors in connection with any systems upgrade or migration to a different hardware or software system, errors or incidents of our cloud providers, bugs or other problems for any of the software we use, either developed in-house or provided by third parties. Security breaches, financial, regulatory or other developments that might prevent these third parties from providing services to us or our users could harm our business. Our systems and our information technology infrastructure are vulnerable to damage or interruption from natural or man-made disasters, power loss, computer viruses, telecommunication and other operational failures, ransomware attacks or any other kind of denial of service related attacks, physical or electronic break-ins, sabotage, intentional acts of vandalism, terrorism, public health crises (including pandemics), extreme weather (including as a result of climate change) and similar events. The public cloud providers could also decide to close their facilities. Any steps that we may take to upgrade and improve the stability and efficiency of our information technology may not be sufficient to avoid defects or disruptions in our technology infrastructure, which could cause a disruption in our business and adversely impact our financial results. Our systems are not fully redundant, and our disaster recovery planning may not be sufficient. Any errors, defects, disruptions, interruptions, delays or cessation of service could result in significant disruptions to our business that could ultimately be more expensive, time consuming and resource intensive than anticipated. We may experience defects or disruptions in our technology infrastructure, including system interruptions and delays that make our site and services unavailable or slow to respond for periods of time, which could adversely impact our ability to fulfill orders, which could reduce our revenue, adversely affect our reputation with or result in the loss of users and negatively impact our financial results. Although we are insured against cyber risks and security breaches up to an annual aggregate limit, our liability insurance may be inadequate and may not fully cover the costs of any claims or damages that we might be required to pay. In the future, we may not be able to obtain adequate liability insurance on commercially desirable or reasonable terms or at all.

In September 2021, we implemented a new version of Titan Cement International’s enterprise resource planning software, SAP, as part of a plan to integrate and upgrade our systems and processes. As we are dependent on the SAP license and system of Titan Cement International, we lack control over system updates, maintenance schedules and overall system management, which could lead to delays or disruptions that impact our operations. The SAP license and system of Titan Cement International might also not fully meet our unique needs, which might make our systems potentially less effective or inefficient. Any of these consequences could have a material adverse effect on our business, results of operations and financial condition.

Our aggregate resource and reserve calculations are estimates and subject to uncertainty.

We estimate aggregate reserves and resources based on available data. The estimates depend upon the interpretation of surface and subsurface investigations, major assumptions and other supporting data, which can be unpredictable.

The quantity must be considered only an estimate until reserves are actually extracted and processed. This uncertainty in aggregate resource and reserve calculation may adversely impact our results of operations.

We may not be able to secure, permit or economically mine strategically located aggregate reserves or locate, permit or operate new ready-mix concrete sites.

As discussed above, aggregates are bulky and heavy and therefore difficult to transport efficiently. Because of the nature of the products, the freight costs can quickly surpass production costs. Therefore, except for geographic regions that do not possess commercially viable deposits of aggregates and are served by rail, barge or ship, the markets for our products tend to be very localized around our quarry sites and are served by truck. New quarry sites often take several years to develop. Our strategic planning and new site development must stay ahead of actual growth. Additionally, we may not be able to locate new ready-mix concrete sites and secure the necessary governmental, operating and environmental permits to operate such new sites. In a number of urban and suburban areas in which we operate, it is increasingly difficult to permit new sites or expand existing sites due to community resistance. Therefore, our future success is dependent, in part, on our ability to accurately forecast future areas of high growth in order to locate

10

__________________________________________________________________________________________________________

optimal facility sites and on our ability to either acquire existing quarries or secure governmental, operating, mining and environmental permits to open new quarries and/or ready-mix concrete sites. If we are unable to accurately forecast areas of future growth, acquire existing quarries or secure the necessary permits to open new quarries and/or ready-mix concrete sites, our financial condition, results of operations and liquidity may be materially adversely affected.

We may not be successful in implementing our growth strategy, which could have a material adverse effect on us.

Our long-term strategy includes both organic growth such as investment in lower carbon products, strengthening of market positions through our vertically integrated business model and digitalization of our operations and growth via acquisitions. We use these strategies to strengthen and develop our existing activities, particularly in growth areas, and as a means of reducing market-specific risk via geographic diversification. The successful implementation of such a growth strategy depends on a range of factors both within and outside of our control.

Any failures to execute our growth strategy or successfully integrate acquired assets and businesses could have a material adverse effect on our business, prospects, financial condition and results of operations.

A large proportion of our business, operations and assets are concentrated in parts of the Eastern Seaboard of the United States.

A large proportion of our business, operations and assets is concentrated in Virginia, Florida, North Carolina, South Carolina and the Metro New York area. Currently, approximately 60% of our operations are concentrated in Florida. Despite positive trends and forecasts for the construction segment’s growth in Florida, there can be no assurance that it will not experience a downturn that will significantly affect our results of operations. For example, the state could experience a decrease in gross domestic product growth, an increase of unemployment or a decrease in consumer confidence, increased property taxes, successive periods of adverse weather conditions, sea level rise or other impacts to infrastructure we rely on, any of which could have a negative effect on our results of operations in Florida. Should positive market trends continue, foreign or national competitors could enter the Florida market to benefit from the increased prices, which could result in a lower market share. There can be no certainty that the positive trends in the U.S. market will continue in the medium- to long-term, in particular given that the U.S. market has been steadily growing since 2011, increasing the risk of a market downturn. Should the U.S. market experience a downturn, demand for our products would decrease. In addition, our kilns could be required to operate at lower utilization rates and the rest of our assets could remain idle because of lower demand.

Failure to achieve and maintain a high level of product quality as a result of our suppliers’ or our manufacturing mistakes or inefficiencies could damage our reputation and negatively impact our revenue and results of operations.

To continue to be successful, we must continue to preserve, grow and capitalize on the value of our brand in the marketplace. Reputational value is based in large part on perceptions of subjective qualities. Even an isolated incident, such as an out of specification product delivered to a construction site, or the aggregate effect of individually insignificant incidents, can erode trust and confidence. In particular, product quality issues as a result of our suppliers’ (including our affiliates’) acts or omissions could negatively impact customer confidence in our brands and our products. As we do not have direct control over the quality of the products manufactured or supplied by such third-party and affiliated suppliers, we are exposed to risks relating to the quality of the products we distribute. If our product offerings do not meet applicable safety standards or customers’ expectations regarding safety or quality, or are alleged to have quality issues or to have caused personal injury or other damage, we could experience lower revenue and increased costs and be exposed to legal, financial and reputational risks, as well as governmental enforcement actions. For example, product quality concerns could result in costly rip and tear expenses for removing previously laid concrete. The termination of key supplier relationships may have a material adverse effect on our business, financial condition and results of operations.

While we regularly test samples of our products before shipment, there can be no assurance that such testing will be adequate to identify all deficient products.

Our financial condition and operations could be adversely impacted by climate change and regulations intended to address climate change.

Severe weather events, such as tornadoes, hurricanes, rain, drought, ice and snowstorms and high- and low- temperature extremes, occur in regions in which we operate and maintain infrastructure. Climate change could change the frequency and severity of these weather events or result in chronic changes to water levels or meteorological patterns, any of which may create physical and

11

__________________________________________________________________________________________________________

financial risks to us. Such risks could have an adverse effect on our financial condition, results of operations and cash flows. Increases in severe weather conditions, extreme temperatures or chronic climatic changes (such as sea level rise or changes in meteorological or hydrological patterns) may also cause infrastructure construction projects to be delayed or cancelled and may limit resources available for such projects, resulting in decreased revenue or increased project costs. Climate change may impact a region’s economic health, which could impact our revenues as our financial performance is tied to the health of the regional economies we serve. For example, if ports or other infrastructure on which we rely become less usable due to climate impacts, it may affect demand for, or our ability to provide, our products.

The price of energy also has an impact on the economic health of communities and our production costs. The cost of additional regulatory requirements related to climate change, such as regulation of greenhouse gas (“GHG”) emissions under the federal Clean Air Act, requirements to replace fossil fuels with renewable energy or to obtain emissions credits or other environmental regulation or taxes could impact the availability of goods and the prices charged by suppliers, which would normally be borne by consumers through higher prices for energy and purchased goods. The costs of such regulations could increase the costs of our products and could adversely impact economic conditions of areas we serve. Such regulations could also increase our cost of doing business by requiring us to install additional pollution control technologies, acquire emissions offsets, or modify or curtail our operations. Various financial market participants also consider climate-related risks in their decision-making. To the extent financial markets believe we are not well positioned to manage any such risk, our ability to access capital markets or to receive competitive terms and conditions could be negatively affected.

Moreover, in certain jurisdictions in which we operate, governmental bodies are increasingly proposing or enacting legislative and regulatory initiatives to address the potential impacts of climate change, such as cap-and-trade systems, limits on GHG emissions and requirements to disclose GHG emissions and other climate change-related information, which are expected to become more stringent in the future. These laws and regulations have the potential to impact our operations directly or indirectly and may result in additional compliance requirements by us. For example, we monitor, analyze and report on GHG emissions from our operations and products in response to laws and customer inquiries. In addition, our manufacturing processes have been and may be affected by new laws and regulations in response to climate change. Compliance with such laws and regulations could have a material adverse effect on our business, financial condition and results of operations.

The cement industry is under increasing regulatory pressure to reduce carbon emissions and achieving significant emissions reductions may involve high costs and technical challenges associated with carbon capture and storage. Due to the uncertain availability of technologies to control GHG emissions and the unknown obligations that potential GHG emission legislation or regulations may create, we cannot determine the potential financial impact on our operations.

In addition, the increasing focus on climate change and stricter regulatory requirements may result in our business facing adverse reputational risks associated with certain of our operations producing GHG emissions. Although we have not yet experienced material difficulties in these areas, if we are unable to satisfy the increasing climate-related expectations of certain stakeholders, we may suffer reputational harm, which may cause the market price of our common shares to decrease, difficulty in accessing the capital or insurance markets or interference with our business operations and ability to make capital expenditures. For further information, please see our risk factor titled “Increasing scrutiny and activism from stakeholders and regulators with respect to ESG matters, including those most relevant to the cement industry, could impact our reputation and the cost of our operations which could adversely affect our business and results of operations.”

Any of the above risks may also impact our customers or suppliers, which could augment existing or result in different risks, including risks that may not yet be known to us.

Our operations are subject to special hazards that have caused in the past and may cause in the future personal injury or property damage, subjecting us to liabilities and possible losses, some of which may not be covered by insurance.

Hauling and ready-mix trucks, particularly when loaded, expose our drivers and others to traffic hazards. Our drivers are subject to the usual hazards associated with providing services on construction sites, while our plant personnel are subject to the hazards associated with moving and storing large quantities of heavy raw materials. Operating hazards can cause personal injury and loss of life, damage to or destruction of property, plant and equipment and environmental damage, and such hazards have in the past, and could result in the future, with us being named in the litigation in the future. Liabilities for such events are difficult to assess and estimate due to unknown factors, including the severity of an injury, the determination of our liability in proportion to other parties, the number of incidents not reported and the effectiveness of our safety program. Provisions for losses are recognized when we have a

12

__________________________________________________________________________________________________________

legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation and a reliable estimate of the amount can be made. If we were to experience claims or costs above our estimates, we might also be required to use working capital to satisfy these claims rather than using the working capital to maintain or expand our operations.

We maintain insurance coverage in amounts and against the risks we believe are consistent with industry practice, but this insurance may not be adequate to cover all losses or liabilities we may incur in our operations.

Our insurance policies are subject to varying levels of deductibles. Where we expect to be reimbursed under an insurance contract, the reimbursement is recognized as a separate asset but only when reimbursement is virtually certain.

We are subject to certain operational risks, including risks regarding safety at work.

Our cement, ready-mix and quarry operations can be hazardous, and factors outside our control, such as weather and temperature, can increase the risks related to those operations. Although we have strict safety policies and training programs intended to systematically educate employees on safety as well as detailed procedures and systems, these programs may fail to prevent all such accidents and, as a result, we have been and could be in the future subject to administrative or legal proceedings arising as a result of breaches of health and safety by our employees, any of which may have an adverse effect on our operations and reputation. The cement production process also generates environmental impacts, including dust, noise or other pollutants, and may require the storage of waste materials. Contamination resulting from waste materials or significant dust, noise or other pollution from site operations could also have the potential of affecting our employees, communities and the environment near our operations, and also negatively affect our business, results of operations and financial condition.

Our customer relationships are not generally governed by long-term agreements, and, as a result, such customers have the right to change the terms under which they do business and/or terminate their relationship with us.

The bulk of our customer relationships are not generally governed by long-term agreements. Consequently, despite the length of our relationships with these customers and our low historical customer turnover rates, there can be no assurance that our customer base will remain stable in the future. If our customers do not renew orders, our business, financial position, results of operations and cash flows could be negatively affected.

Relationships with our customers are based on and involve a high degree of trust that the customer(s) will continue to transact with us for a long period of time. However, under certain of these agreements, we would have no recourse against certain customers if they are determined to terminate the agreement or they utilize other service providers that may compete with us. These customers could additionally underperform, not perform at all under these agreements and even walk away entirely. Our lack of recourse and ability to prevent customers from walking away from our agreements could have a material effect on our financial performance.

Our business is based in part on government-funded infrastructure projects and building activities, and any reductions or reallocation of spending or related subsidies in these areas could have an adverse effect on us.

We often serve as a subcontractor and depend on government spending for infrastructure and other similar building activities. As a result, demand for some of our products is influenced by local, state and federal government fiscal policies, tax incentives and other subsidies and other general macroeconomic and political factors. Projects in which we participate may be funded directly by governments or privately funded but are otherwise tied to or impacted by government policies and spending measures.

Government spending is often approved only on a short-term basis and some of the projects in which our products are used require longer-term funding commitments. If government funding is not approved or funding is lowered as a result of poor economic conditions, lower than expected revenues, competing spending priorities or other factors, it could limit infrastructure projects available, increase competition for projects, result in excess inventory and decrease sales, all of which could adversely affect our profitability.

Additionally, certain regions or states may require or possess the means to finance only a limited number of large infrastructure projects and periods of high demand may be followed by years of little to no activity. There can be no assurances that governments will sustain or increase current infrastructure spending and tax incentive and other subsidy levels, and any reductions thereto or delays therein could affect our business, liquidity and financial condition and results of operations.

13

__________________________________________________________________________________________________________

If we are unable to accurately estimate the overall risks, requirements or costs when we bid on or negotiate contracts that are ultimately awarded to us, we may achieve lower than anticipated profits or incur contract losses.

Even though the majority of our contracts for public projects as a subcontractor contain raw material escalators to protect us from certain input material price increases, a portion of the contracts are often on a fixed cost basis. The costs incurred and profit realized, if any, on our contracts can vary, sometimes substantially, from our original projections due to a variety of factors, including, but not limited to: failure to include materials or work in a bid, or the failure to estimate properly the quantities or costs needed to complete a lump sum contract; delays caused by weather conditions or otherwise failing to meet scheduled acceptance dates; contract or project modifications or conditions creating unanticipated costs that are not covered by change orders; changes in availability, proximity and costs of materials, including cement, aggregates and other construction materials, as well as fuel and lubricants for our equipment; to the extent not covered by contractual cost escalators, variability and inability to predict the costs of purchasing coal, diesel, natural gas and cement; availability and skill level of workers; fraud, theft or other improper activities by our suppliers, subcontractors, designers, engineers, customers or our own personnel; failure by our suppliers, subcontractors, designers, engineers or customers to perform their obligations; mechanical problems with our machinery or equipment; citations issued by any governmental authority, including the Occupational Safety and Health Administration (“OSHA”) and Mine Safety and Health Administration (“MSHA”); difficulties in obtaining required governmental permits or approvals; changes in applicable laws and regulations; uninsured claims or demands from third parties for alleged damages arising from the design, construction or use and operation of a project of which our work is part; and public infrastructure customers may seek to impose contractual risk-shifting provisions more aggressively which may result in us facing increased risks.

These factors, as well as others, may cause us to incur losses, which could have a material adverse effect on our financial condition, results of operations and liquidity.

Our industry is capital intensive, and we have significant fixed and semi-fixed costs. Therefore, our profitability is sensitive to changes in volume.

The property and machinery needed to produce our products can be very expensive. Therefore, we need to spend a substantial amount of capital to purchase and maintain the equipment necessary to operate our business. Although we believe that our current cash balance, along with our projected internal cash flows and our available financing resources, will provide sufficient cash to support our currently anticipated operating and capital needs, if we are unable to generate sufficient cash to purchase and maintain the property and machinery necessary to operate our business, we may be required to reduce or delay planned capital expenditures or incur additional debt. In addition, given the level of fixed and semi-fixed costs within our business, particularly at our cement production facility, decreases in volumes could negatively affect our financial position, results of operations and liquidity.

An inability to successfully identify, consummate and integrate acquisitions, divestitures and other significant transactions could have an adverse impact on our business and financial results.

A portion of our historical growth has occurred through acquisitions, and we will likely execute acquisition transactions in the future. Acquisitions involve risks including, among other things, that the businesses acquired will not perform as expected. We are presently evaluating, and we expect to continue to evaluate on an ongoing basis, possible acquisition transactions. We are presently engaged, and at any time in the future we may be engaged, in discussions or negotiations with respect to possible acquisitions, including larger transactions that would be significant to us. We regularly make, and we expect to continue to make, non-binding acquisition proposals, and we may enter into letters of intent, in each case allowing us to conduct due diligence on a confidential basis. There can be no assurances that we will be able to recover the current carrying amount of our investments, and in some circumstances, assets or businesses may result in additional impairment expenses or other losses. In addition, we may become subject to certain contractual indemnity or other obligations or may fail to successfully deploy sale proceeds. We cannot predict the timing of any contemplated transactions. To successfully acquire a significant target, we may need to raise additional capital through additional equity issuances, additional indebtedness or a combination of equity and debt issuances. Our results of operations from these acquisitions could, in the future, result in impairment charges for any of our intangible assets, including goodwill or other long-lived assets, particularly if economic conditions worsen unexpectedly. As a result of these changes, our financial condition, results of operations and liquidity could be materially adversely affected. There can be no assurance that we will enter into definitive agreements with respect to any contemplated transactions or that they will be completed. Our acquisitions and portfolio optimization efforts have placed, and may continue to place, significant demands on our management and operational and financial resources.

14

__________________________________________________________________________________________________________

Acquisitions may require integration of the acquired companies’ sales and marketing, distribution, production, purchasing, information technology, finance and administrative organizations. We may not be able to integrate successfully any business we may acquire or have acquired into our existing business and any acquired businesses may not be profitable or as profitable as we had expected. Factors affecting the successful integration of acquired businesses include, but are not limited to, the following: we may become liable for certain, and potentially significant, liabilities of any acquired business, whether or not known to us; substantial attention from our executive management and the management of the acquired business may be required, which could decrease the time that they have to service and attract customers; capital equipment at acquired businesses may require additional maintenance or need to be replaced sooner than we expected; the complete integration of acquired companies depends, to a certain extent, on the full implementation of our financial systems and policies; and the ability to retain key employees. Our inability to complete the integration of new businesses in a timely and orderly manner could increase costs and lower profits.

A lowering or withdrawal of the ratings, outlook or watch assigned to our business or our debt by rating agencies or the credit rating of Titan Cement International may increase our future borrowing costs and reduce our access to capital.

Titan Cement International both provides intercompany loans to us and guarantees our third-party debt. Any change in the credit rating of Titan Cement International, which is out of our control, could have a material adverse effect on our ability to borrow and our cost of capital.

The rating, outlook or watch assigned to Titan Cement International or to our debt could be lowered or withdrawn entirely by a rating agency if, in that rating agency’s judgment, current or future circumstances relating to the basis of the rating, outlook or watch such as adverse changes to Titan Cement International’s or our business, so warrant. Additionally, we do not have credit history without the guarantee of Titan Cement International. Without an operating history, we may be unable to or find it difficult to obtain our own credit score. Our credit ratings may also change as a result of the differing methodologies or changes in the methodologies used by the rating agencies. Any future lowering of our debt’s ratings, outlook or watch likely would make it more difficult or more expensive for us to obtain debt financing.

Holders of our common shares will have no recourse against us or any other parties in the event of a change in or suspension or withdrawal of such ratings. Any lowering, suspension or withdrawal of such ratings may have a material adverse effect on the market price or marketability of our common shares.

Our ability to repay or refinance our indebtedness on time and distribute dividends and share capital to our shareholders depends upon our future cash flows from operations, as well as prevailing market conditions.

Our indebtedness primarily consists of intercompany loans, short-term bank borrowings and lease liabilities.

Our ability to make payments on and refinance our indebtedness and to fund working capital, capital expenditures and other expenses will depend on our future operating performance and ability to generate cash from operations. Our ability to generate cash from operations is subject, in large part, to general economic, competitive, legislative and regulatory factors and other factors that are beyond our control. We may not be able to generate sufficient cash flow from operations or obtain enough capital to service our debt or fund our planned capital expenditures.

Similarly, we are a holding company and our ability to repay our debt, pay dividends or make other contributions to our shareholders depends on our subsidiaries’ ability to pay cash to us pursuant to dividend payments and/or other obligations. The ability of our subsidiaries to pay dividends to us in the future will depend on their earnings, covenants contained in future financing or other agreements and on regulatory restrictions. Similarly, we may be unable to distribute dividends in order to maintain our credit rating and avoid any potential credit downgrade. Thus, we may not have sufficient funds to pay our debt or distribute dividends.

Our ability to refinance our debt will depend in part on our financial position at such time. Any refinancing of our debt could be at higher interest rates than our current debt and may require us to comply with more onerous covenants, which could further restrict our business operations. In particular, certain intercompany loans and credit facilities with Titan Global Finance PLC (“TGF”), are based on financial terms contained in the arm’s length agreements consummated among TGF and its third party lenders. There is no guarantee that TGF will be willing to continue to enter into debt agreements with us on similar terms or at all. Refinancing such debt with third parties may increase our cost of capital and may subject us to more onerous covenants. The terms of existing or future debt instruments may restrict us from adopting some of these alternatives.

15

__________________________________________________________________________________________________________

The economic environment has in the past been marked by a scarcity of financing for periods of time, in particular with regard to long-term financing. If financial and economic conditions were to deteriorate, including as a result of political and economic uncertainty or instability, or if interest rates were to increase, it may be more costly and more difficult for us to access new credit or to refinance our debts on terms that are acceptable to us, or at all. This could have a material adverse effect on our business, results of operations and financial condition.

We are exposed to risk of loss resulting from the nonpayment and/or nonperformance by our customers and counterparties.

Our customers include public and private entities that have been, and may continue to be, negatively impacted by the changing landscape in the global economy. A recessionary construction economy can increase the likelihood that we will not be able to collect on all accounts receivable or may experience a delay in payment from some customers. If our customers or counterparties experience financial difficulties, which has occurred and may reoccur, we could experience difficulty in collecting receivables. We face collection risk as a normal part of business where we perform services and subsequently bill clients for such services. In the event that we have concentrated credit risk from clients in a specific geographic area or industry, continuing negative trends or a worsening in financial conditions in that specific geographic area or industry could make us susceptible to disproportionately high levels of default. Nonpayment and/or non-performance by our customers and counterparties could have a negative impact on our results of operations and cash flows.

Fluctuations in foreign exchange rates may have an adverse effect on our business.

We have foreign exchange rate risk as a result of euro-denominated fixed-rate loans and short-term euro-denominated variable rate loans. We enter into foreign exchange derivatives with notional amounts closely aligned with the underlying borrowings, but cannot be assured that our hedging will adequately protect us against foreign exchange fluctuation risk. If the U.S. dollar weakens as compared to the euro, our cost of capital will increase, and our business may be adversely affected.

We are subject to impairment losses related to non-financial assets.

The cement, aggregates and, to a lesser extent, other construction materials business is capital intensive. Due to the heavy weight of the product and our high distribution costs, shifts in local markets and/or product ranges might lead to impairment of the assets concerned as the investment in those assets may not yield the return that was expected when the investment was made. Impairment losses impact negatively on profitability and equity.

We may fail to retain and attract qualified and skilled employees, including management, engineering and technical personnel, or fail to maintain satisfactory labor relations with our unions.

While we aim to attract and retain the best possible candidates from domestic and international markets, we may be unable to recruit and retain experienced, capable and reliable personnel, especially senior and middle management and skilled technical personnel with appropriate professional qualifications. If members of our executive management team were to depart, we might not be able to implement a successful succession program in a timely manner, if at all. Additionally, without a sufficient number of skilled employees, our operations and manufacturing quality could suffer. The resulting labor shortages, as well as competition from other industries, or other factors, could increase our labor costs and could negatively affect our results of operations.

From time to time, we enter into discussions and collective bargaining agreements with labor unions, which represent less than five percent of our workforce as of December 31, 2024. Although we maintain good relations with our unions and have not faced a material strike that affected our operations, there can be no assurance that we will not experience labor unrest, difficulty in negotiating collective bargaining agreements or disputes or actions in the future, some of which may be significant and could adversely affect our business, prospects, financial condition, reputation and results of operations.

Artificial intelligence presents risks and challenges that can impact our business by posing security risks to our confidential information, proprietary information and personal data.

Issues in the development and use of artificial intelligence, combined with an uncertain regulatory environment, may result in reputational harm, liability or other adverse consequences to our business operations. As with many technological innovations, artificial intelligence presents risks and challenges that could impact our business. We work with vendors that incorporate artificial intelligence tools into their offerings and the providers of these artificial intelligence tools may not meet existing or rapidly evolving regulatory or industry standards with respect to privacy and data protection and may inhibit our or our vendors’ ability to maintain an

16

__________________________________________________________________________________________________________

adequate level of service and experience. If we, our vendors, or our third-party partners experience an actual or perceived breach or privacy or security incident because of the use of generative artificial intelligence, we may lose valuable intellectual property and confidential information and our reputation and the public perception of the effectiveness of our security measures could be harmed. Further, bad actors around the world use increasingly sophisticated methods, including the use of artificial intelligence, to engage in illegal activities involving the theft and misuse of personal information, confidential information and intellectual property. Any of these outcomes could damage our reputation, result in the loss of valuable property and information and adversely impact our business.

Risks Related to Our Relationship with Titan Cement International

We plan to rely on functions, systems and infrastructure provided by Titan Group, and if Titan Group fails to perform these transitional services we may fail to replicate or replace them.

Since our inception, we have received services from Titan Group and will continue to receive services under the Shared Services Agreement from Titan Group. Under the Shared Services Agreement, Titan Group has agreed to continue to provide us with certain services currently provided to us by or through Titan Group. The Shared Services Agreement does not continue indefinitely and will last for five years with an option to renew for additional two-year periods, and services provided under the Shared Services Agreement may generally terminate at various times specified in the agreement and the schedules thereto.

If Titan Group ceases to provide these services to us, either as a result of the termination of the Shared Services Agreement or individual services thereunder or a failure by Titan Group to perform its obligations under the Shared Services Agreement, our costs of performing or procuring these services or comparable replacement services could increase as a result of replicating the services ourselves or contracting with a third-party for the services at a higher cost.

There is a risk that an increase in the costs associated with replicating and replacing the services provided to us by Titan Group under the Shared Services Agreement, or continuing to provide services to Titan Group, and the diversion of management’s attention to these matters could have a material adverse effect on our business, results of operations, financial condition and liquidity. We may fail to replicate the services we currently receive from Titan Group on a timely basis, without interruption to or degradation of ongoing operations, or at all, which may put further constraints on our human resources, capital and other resources that are simultaneously working on the retention and replacement of the services and ongoing efforts to implement new technological developments and innovations; such additional constraints could jeopardize our ability to execute on any one of these specific work streams. In addition, Titan Group will be working on similar initiatives which may impact the level and quality of transition services we receive from them. Additionally, we may not be able to operate effectively if the transition to the replacement services causes interruptions to or degradation of operations or the quality of replacement services is inferior to the services we are currently receiving.

Titan Cement International and its subsidiaries are among our largest material and service providers, and we might have received better terms from unaffiliated third parties than under our agreements with Titan Cement International and its subsidiaries.